Content

In September 2023 I put £40 on the Florida Panthers to win the Stanley Cup at 14/1, and I’ll never forget the look on my flatmate’s face when I told him. Florida had just lost in the Final, the Vegas Golden Knights were the reigning champions, and the betting markets had Florida priced as a fading contender. Eight months later they won the Cup. The next year they did it again. That £40 ticket was the moment Stanley Cup futures stopped being a once-a-year flutter for me and started being a market I trade on a rolling calendar, with the same discipline I use for puck lines and props.

A Stanley Cup futures bet is a long-dated wager on which team will lift the Cup at the end of the NHL season. It’s a different animal from a match bet — the price moves continuously from opening night to the Final, the variance is enormous, and the rewards are calibrated to the size of the field. Where a moneyline gives you fifteen to forty percent edges to chase on a single night, a futures market hands you a season-long position that can be hedged, partially cashed out, or held to settlement. That structural difference is why I treat futures as a separate bankroll inside my NHL strategy, and why I think every UK bettor who follows the league seriously should have at least one ticket in play through any given winter.

The numbers right now tell the story. The Edmonton Oilers opened the 2025/26 season as the bookmakers’ favourites at +650, with Florida — the team I keep coming back to — close behind at +750 after their back-to-back Cups in 2024 and 2025. Those opening prices are the starting point. Where the market goes from there, and where the value lives at each stage of the calendar, is what this guide is built to walk you through.

How the Futures Market Actually Breathes

The mechanics of a futures market are nothing like the mechanics of a moneyline, and that’s the first thing a UK bettor coming from football has to internalise. A moneyline closes within minutes of puck drop. A futures market opens in June and breathes for a full eleven months, reacting to free agency, training camp news, October scoring runs, December slumps, trade-deadline reshuffles and playoff matchups. Every one of those events is a price-moving event, which means the entry point you choose matters more than almost anything else about the ticket.

When markets open

Most UK bookmakers open Stanley Cup futures for the next season within a week of the previous Cup being awarded. The 2025/26 markets opened at the major operators in late June 2025, days after Florida finished off their second straight title. Those opening prices are deliberately conservative — the book hasn’t yet seen training-camp news, free-agency results or pre-season form, so they post wider, more cautious lines that protect against early sharp action. That window between the Cup ceremony and the opening of the next season’s market is where the long-shot prices are at their longest, and where contenders are priced before any of the bullish news of summer arrives to compress them.

How prices move through the season

Futures pricing typically sits in a band from +650 to +900 on the clear contenders and pushes out to +5000 or longer on the rebuild teams and unfancied dark horses. Those numbers aren’t static — a contender who wins twelve of their first fifteen games will compress from +800 down to +450 inside a month, and a presumed rebuild team that surprises through October can swing from +6000 to +2500 on momentum alone. The market moves both on results and on perception, which is the part bettors who only trade match markets find hardest to swallow. A team can play exactly the same hockey for two weeks and have their futures price shift twenty percent because public money has moved.

Trade deadline impact

The single most violent moment in the futures calendar is the NHL trade deadline in early March. Two or three contenders will load up with rentals — a top-six forward, a defensive defenceman, sometimes a backup goalie — and their futures prices will compress sharply. The teams that fail to land their targets, or whose acquisitions underwhelm the market, drift in the opposite direction. The window of about ninety-six hours either side of the deadline is the second-best entry point for futures, after the opening summer window — the books are reacting in real time, the public is reacting on emotion, and the gap between price and probability gets wider than at any other point in the season.

Decoding the Price You See on Your Screen

I sat next to a friend in a pub in north London last March while he tried to figure out what 12/1 actually meant for his Edmonton futures ticket. He had bet at a UK-licensed sportsbook on his phone, taken the fractional price without thinking, and was now trying to work out his potential return after the Oilers had compressed to 6/1. The conversation took longer than it should have, and not because he wasn’t sharp — it was because fractional pricing on long-shot futures hides a layer of maths that decimal pricing exposes immediately. Understanding the notation is the difference between knowing what your ticket is worth and guessing.

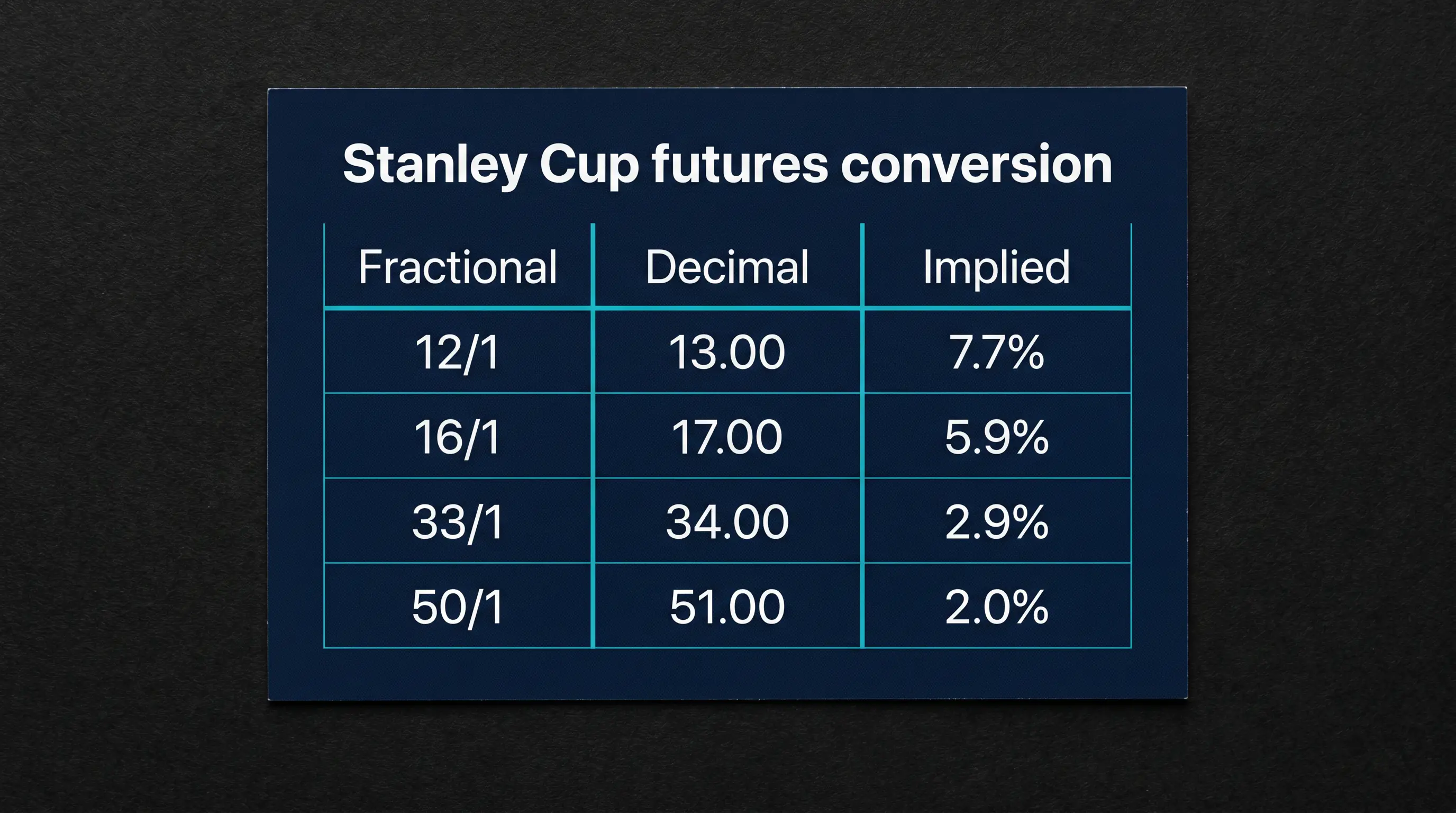

UK fractional futures — what 12/1 means

A 12/1 fractional price means you receive twelve units of profit for every one unit you stake, plus your stake back. A £10 bet at 12/1 returns £130 total — £120 profit and your £10 stake. The implied probability is one divided by thirteen, or about 7.7 percent. UK books default to fractional notation across all their futures markets, and the fractions get unwieldy as the lines get longer — 50/1, 100/1, sometimes 250/1 on genuine longshots. The convention works fine for short prices like 5/2 or 7/4, but on a 33/1 ticket the rounding can hide three or four cents per pound of value compared to the underlying decimal price the book’s model is using.

Decimal futures and exchanges

Decimal pricing is what most professional traders default to because it’s mathematically cleaner. A 12/1 fractional price converts to 13.00 decimal — your stake multiplied by 13.00 is your total return. The implied probability is the reciprocal of the decimal price, so 13.00 is 1/13 = 7.7 percent, the same as before. Betting exchanges like Betfair quote everything in decimal by default, and the prices on the exchange will sometimes differ from the bookmaker’s fractional version by a noticeable margin. On a 16/1 fractional, which is 17.00 decimal, the same ticket on the exchange might be matched at 18.5 or 19.0 depending on how the market is weighted. Comparing the fractional offered by the book against the decimal available on the exchange is the cleanest value check a UK futures bettor can run.

Converting long-shot prices

Long-shot futures are where the maths gets interesting. A 50/1 fractional is 51.00 decimal, or 1.96 percent implied probability. A 100/1 fractional is 101.00 decimal, or 0.99 percent. The compression at the long end of the market is real — moving a price from 50/1 to 33/1 represents a probability shift from 1.96 percent to 2.94 percent, which is a fifty-percent jump in the team’s perceived chances. That’s why a longshot ticket can look like an absurd lottery line in June and a reasonable position by January. Understanding the conversion is what lets you size the bet correctly — a 50/1 at £20 represents a position you’d be happy to ride if the price compresses to 12/1 by March, but only if you’ve understood that twelve-to-one represents an implied probability four times larger than fifty-to-one.

The Contender-Longshot Trade-Off, Calibrated

Every futures portfolio I’ve run has at least one contender position and at least one longshot. Stacking only contenders gives you the worst variance-to-payout ratio in betting — you bet five teams at sub-1000 implied prices, and if any one of them wins the Cup you make roughly your stake back. Stacking only longshots gives you a heroic story to tell once every five years and four seasons of frustration in between. The right mix sits between the two, and the proportion depends on the structural realities of the league right now.

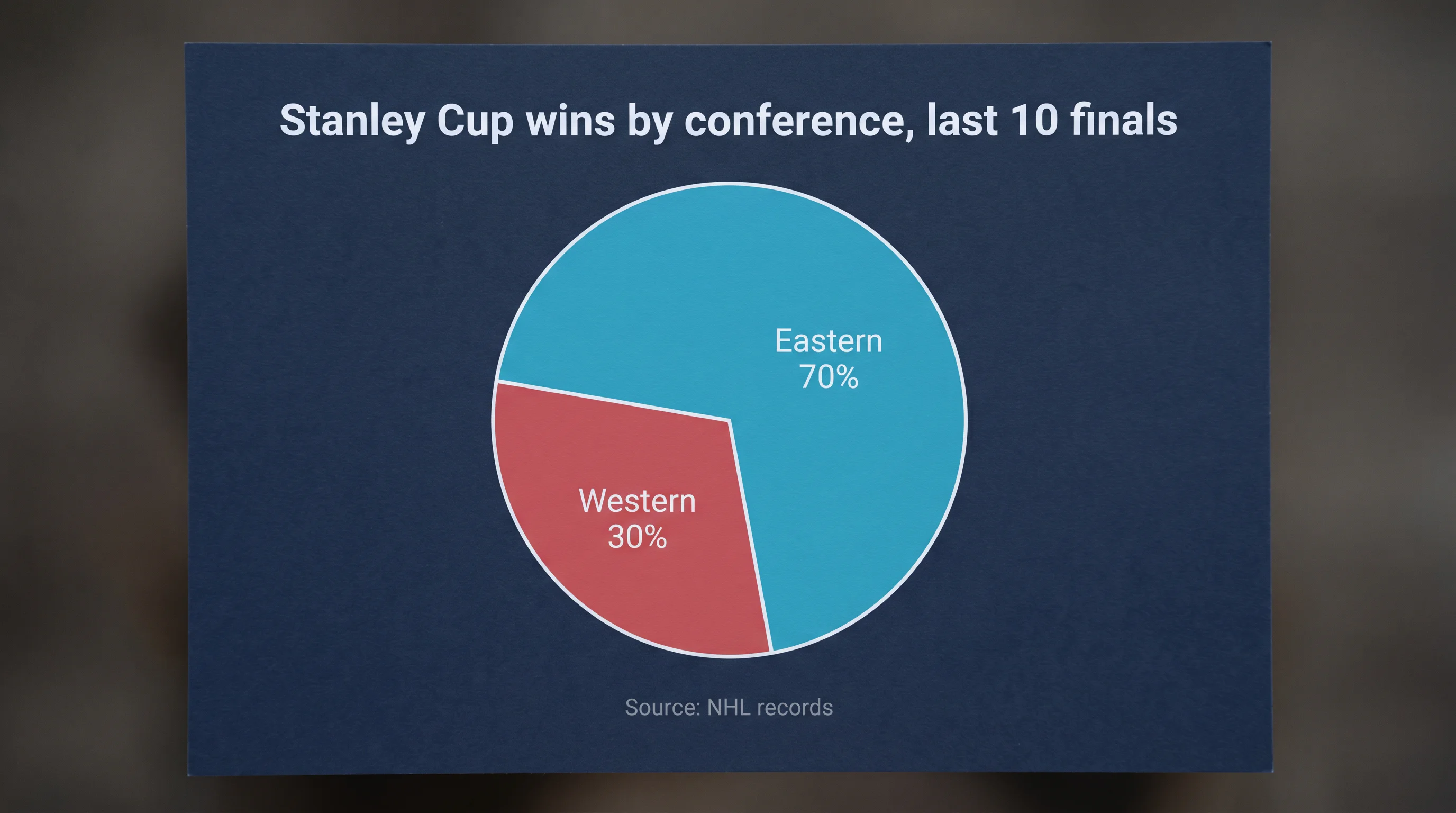

The eastern conference bias

Across the last ten Stanley Cup Finals, seventy percent of the winning teams have come from the Eastern Conference. That number isn’t a coincidence — it tracks the concentration of elite goaltending and defensive depth in the East, and the way the playoff bracket structure means an Eastern team often plays one fewer high-level series than a Western counterpart to reach the Final. Florida, Tampa Bay, Pittsburgh, Washington — the recent Cup history is heavily weighted east. When I build a futures portfolio, I deliberately overweight Eastern teams in the under-2000 price band, because the structural prior says they’re seventy-percent likely to be in the Final regardless of which Western team makes it through.

Backing the perennial favourites

The Florida Panthers winning the Cup in 2024 and 2025 wasn’t a coincidence either. Modern NHL champions tend to repeat — the same nucleus of players, coaching staff and goaltending profile carries from one Cup run to the next. Edmonton was the favourite for 2025/26 at +650 partly because of Connor McDavid’s individual brilliance and partly because the roster had been pushed to the Final two seasons running and was theoretically primed for a third attempt. Florida at +750 was the perennial-favourite play built on the back of two straight Cups, an intact core, and the assumption that the formula would keep working. Backing perennial favourites is the lowest-variance way to engage with futures — the prices are tight, the implied probabilities are honest, and the downside is that the payouts are modest by futures standards.

Hunting longshot value

Longshot futures live in the +5000-and-up band, and they reward bettors who can identify structural changes the market hasn’t priced. A team that hires a new head coach in May, signs a number-one goalie in July, and trades for a top-pairing defenceman in August is a fundamentally different team than the one the opening odds were priced on. If the book hasn’t repriced aggressively enough between those moves, you can buy a +5000 ticket on a team whose true probability is closer to two percent rather than the implied two-tenths. The trade-off is variance — you’ll be wrong four years out of five — but the asymmetric payoff means even a single longshot landing across a five-year window covers the losing tickets and then some.

Knowing When to Take the Money Off the Table

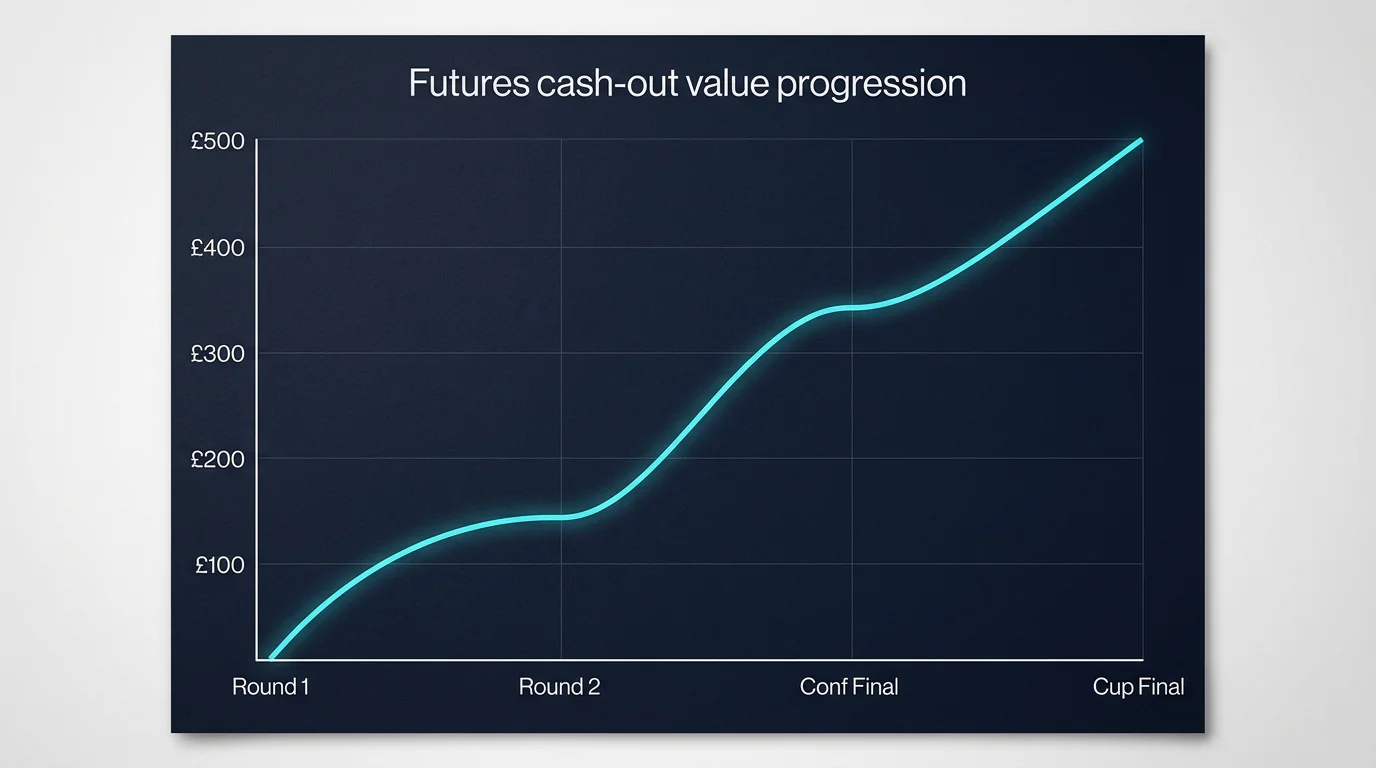

The hardest decision I make in any futures ticket isn’t when to bet — it’s when to stop holding. A £40 ticket on Florida at 14/1 in September 2023 was worth roughly £560 at one point during their 2024 playoff run. I held it. They won. I cashed the full ticket. The next April, I had a different £30 ticket at 18/1 that swung to a peak value of £420 during the Conference Finals, and I cashed out half at £200 because the goalie I’d been depending on had just left a game injured. The team got eliminated in the next round. Both decisions were correct given the information I had at the time, and the framework I use for futures cash-out is the most under-discussed skill in the whole market.

When to hedge in the playoffs

Hedging is the act of placing a bet on the other side of your futures position to lock in a guaranteed profit regardless of outcome. The classic case: you’ve backed Team A at 20/1 for £20 in October. By the Conference Final, Team A is into the Stanley Cup Final and priced at evens. You can place a £200 bet on Team B in the Final at evens, and now both outcomes return roughly the same profit — £180 if A wins (£420 from the original ticket minus the £200 hedge plus the £200 stake) or £200 if B wins. The exact maths depends on the prices and stakes, but the principle is that a hedge converts a high-variance position into a low-variance lock. Whether you should hedge depends on your bankroll exposure and your read on the matchup — there’s no universal answer, only a personal one.

UK bookmaker cash-out features

Every major UK bookmaker now offers cash-out on Stanley Cup futures, which is effectively the book offering you a hedge they’ve priced themselves. The cash-out value is always less than the full theoretical hedge value, because the book is taking margin on the early settlement. On a £20 ticket at 14/1 with a current price of 4/1, the implied book payout would be £100, but the cash-out offer might come in at £85 or £88 depending on the operator’s margin policy. The trade-off is convenience versus value — taking the cash-out is one tap on a phone, building a hedge yourself requires placing a second bet at a different price and tracking both positions. I cash-out when the margin loss is small and the matchup risk is high. I hedge manually when the cash-out feels too punitive.

Locking in profit before the Final

The moment to seriously consider locking profit is when your team has reached the Conference Final and the other side is a goalie-heavy matchup against a hot opponent. This year’s Stanley Cup Final between Vegas and Carolina is the textbook example — going into the series, anyone holding a Vegas futures ticket from earlier in the season had a decision to make about whether to take a hedge on Carolina at the available Final price or ride for the full payout. There’s no shame in cashing a portion at the Conference Final stage and letting the rest ride. The discipline is acknowledging that a one-in-two series outcome means your equity in the ticket is roughly half of its full-settlement value, and behaving accordingly.

The Futures Errors That Drain Bankrolls Quietly

Across nine seasons of running futures portfolios, I’ve made every mistake on the list once and a couple of them twice. The pattern is always the same — small individual errors that compound into a losing year because the underlying structure of the portfolio was wrong from the start. Futures don’t drain a bankroll the way a bad parlay night does. They drain it slowly, across months, through positions that looked sensible in October and quietly went to zero in April.

Betting too many longshots

The most common error is over-stacking the longshot side of the book. Five tickets at 40/1 each on five different teams is twenty times the variance of one ticket at 8/1 on a single contender, and the probability that any of the five longshots wins is still less than the probability that the single 8/1 contender does. Longshots feel cheap because the individual stake is small, but five £10 tickets at 40/1 is a £50 position with a sub-twelve-percent probability of returning anything at all. The fix is to treat your total futures stake as a fixed allocation and ensure no more than thirty percent of it is in tickets priced longer than 20/1.

Ignoring goalie injuries

A starting goaltender going down with a long-term injury can erase a futures position overnight, and the bettors who don’t track injury reports are the ones who get caught. When Vasilevskiy missed the start of the 2023/24 season for Tampa Bay, the futures price on the team drifted from 12/1 to 22/1 inside a week. Anyone holding a long position who hadn’t checked the injury report was sitting on a ticket whose true value had nearly halved. The fix is operational — check the NHL injury board the morning of any deadline-style decision, and price your existing futures positions accordingly.

Overweighting regular-season storylines

The third error is letting the narrative of a great regular season convince you the team is a true contender. Regular-season records and playoff success are loosely correlated at best, and the highest-finishing team in the standings has won the Cup in only a small minority of recent seasons. Betting futures on a team because they’re 35-12-5 in early February is the same logic that loses money on Presidents’ Trophy bets — the regular-season story is not the playoff story. We’ll get to the specific maths on that mismatch in the next section, because it deserves its own treatment.

The Presidents’ Trophy Trap

NHL Commissioner Gary Bettman said something during a CNBC interview in November 2025 that captured the modern futures market better than any analyst ever has: “We have aligned with the prediction market because we believe our fans need to understand that if they’re going to execute those contracts, it’s based on real data.” Real data. That’s the line that should sit above every futures bettor’s screen, because the data on the regular season’s relationship to the Stanley Cup is brutal — and most futures bettors ignore it.

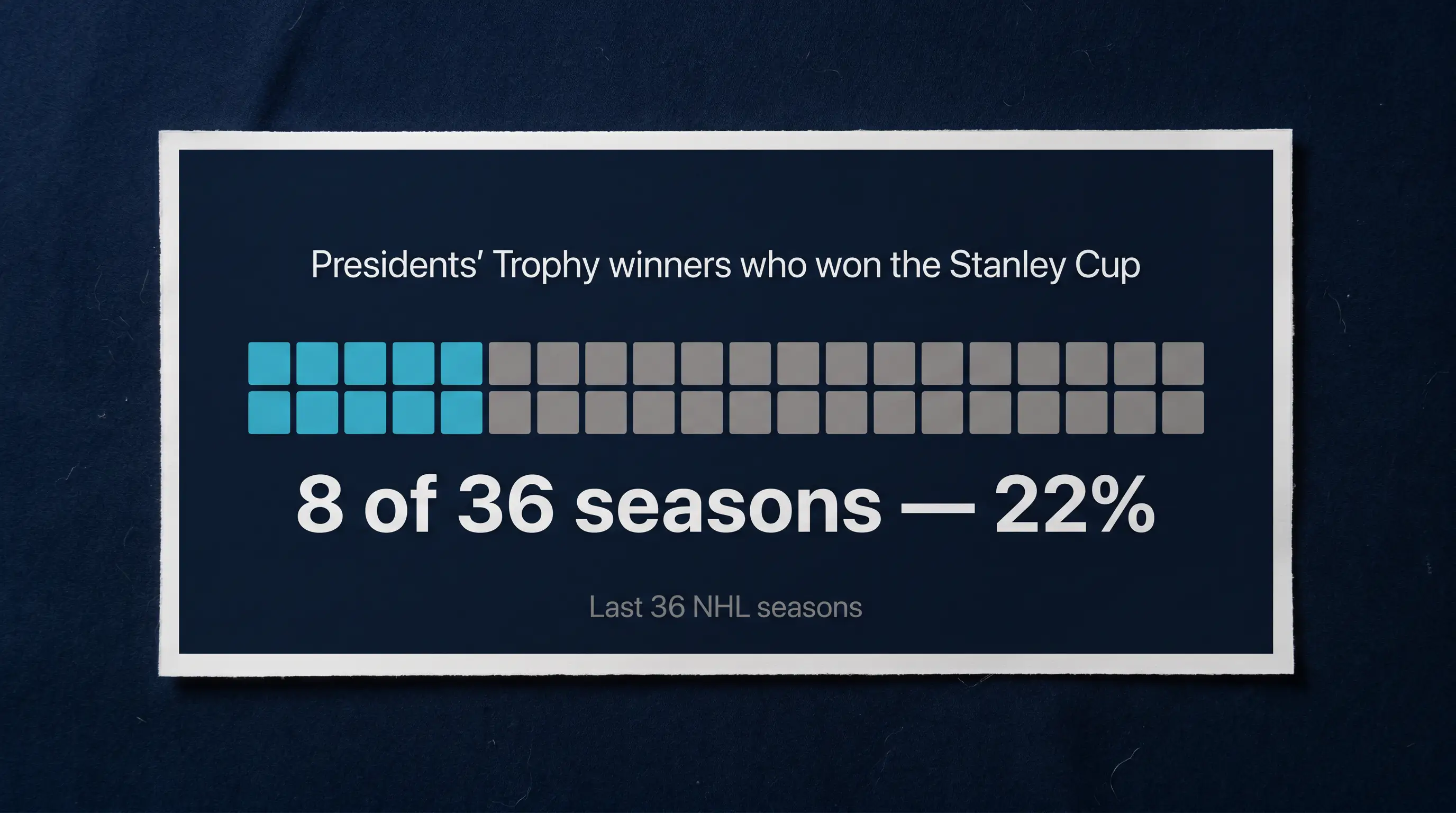

The 8-from-36 problem

Across the last thirty-six NHL seasons, the Presidents’ Trophy winner — the team that finishes the regular season with the most points — has gone on to win the Stanley Cup only eight times. Eight from thirty-six. That’s a twenty-two-percent strike rate for the team the market spends six months calling the favourite. The implication for futures is severe: the team trading at the shortest price in March is overpriced by the structural reality of playoff hockey, and a contrarian position on a second-tier contender at 8/1 or 10/1 is often better value than the chalk at 5/1.

Why best regular-season teams flame out

The reasons aren’t mysterious. Regular-season hockey rewards depth, durability and special-teams efficiency across eighty-two games. Playoff hockey rewards goaltending, top-six skill and matchup-specific coaching across four series. The skill sets only partially overlap. A team that scores at 3.6 goals per game in the regular season can be neutralised by a single hot goalie in round one, and the entire futures investment on that team evaporates in a six-game series. The fix isn’t to ignore the Presidents’ Trophy contender — it’s to recognise that their March price is built on regular-season inputs and should be adjusted heavily downward for the playoff context.

Adjusting your futures stance after February

The window between the trade deadline in early March and the start of the playoffs in mid-April is when I do my heaviest futures repositioning. I sell out of inflated regular-season chalk via cash-out, redistribute the stake into matchup-specific Conn Smythe and goalie-specific positions, and build a hedge structure that locks profit on the original ticket while opening exposure to the right side of round one. The Conn Smythe market — the individual playoff MVP award — moves in lockstep with Stanley Cup futures, and the relationship between team futures and individual award futures is worth understanding in depth. For the full breakdown on how I trade individual playoff award markets alongside Cup futures, my Conn Smythe trophy guide walks through the timing windows and which player profiles consistently outperform their pre-playoff prices.

How I Stage My Stanley Cup Futures Across the Calendar

The framework that has kept me profitable on Stanley Cup futures across the last nine seasons isn’t a betting system — it’s a calendar. Three windows, three distinct sizing rules, one continuous portfolio. The opening window in late June through August is when I take my long positions on contenders and the speculative longshot tickets that need a full season to mature. The mid-season window from late October through the All-Star break is when I reassess and add small positions on teams whose openings I missed. The deadline window in early March is when I do my heaviest repositioning, taking partial cash-outs on inflated chalk and adding directional positions on teams that have just acquired the right pieces.

Across those three windows the goal is the same — to hold at least one position with meaningful upside into the playoffs, while never having more than fifteen percent of my total NHL bankroll tied up in futures at any one moment. Futures discipline is bankroll discipline first and price discipline second. Get the sizing right and the price reads take care of themselves. Get the sizing wrong and even a winning ticket can’t compensate for the losing ones around it.

Stanley Cup futures gave me my best single ticket in nine years of NHL betting with that Florida 14/1 in 2023, and they’ve given me my most expensive losing portfolio in a year I’d rather not relitigate. The market rewards patience, calendar awareness and the willingness to cash out before the variance closes the door. Treat the season as one long futures trade rather than a sequence of match bets, and the Stanley Cup futures market stops being a once-a-year flutter and starts being one of the most rewarding corners of NHL betting on offer.

When do UK bookmakers typically open Stanley Cup futures for the next season?

Major UK bookmakers open Stanley Cup futures markets within a week of the previous season’s Cup being awarded — usually mid to late June. The opening prices are deliberately conservative because the book has not yet seen training-camp news, free-agency results or pre-season form. The opening window through to early September is when contender prices are at their longest, and where bettors who follow off-season news closely tend to find the best entry points before the market compresses on autumn results.

Can I cash out a Stanley Cup futures bet before the playoffs end?

Yes, every major UK bookmaker offers cash-out on Stanley Cup futures, including during the playoffs. The cash-out offer will be less than the full theoretical hedge value because the book takes a margin on the early settlement. The offer updates continuously as the team’s chances change — a strong playoff run will push the cash-out value up, an injury or a loss will pull it down. Cash-out is most useful when you want to lock guaranteed profit and the margin loss versus a manually constructed hedge is small.

What happens to my futures bet if the team I picked is eliminated early?

A Stanley Cup futures bet settles as a loss the moment the team is eliminated from playoff contention — either by missing the playoffs entirely or by losing their last playoff series. There is no partial settlement and no refund. The stake is lost in full. This is why position-sizing and longshot allocation matter so much in futures — the binary settlement structure means every losing ticket goes to zero, regardless of how close the team came.

Is it better to bet futures pre-season or wait until the NHL trade deadline?

Both are sharp windows, but they reward different bettors. Pre-season futures offer the longest prices and the most uncertainty — strong if you’ve done deep off-season research on roster moves and coaching changes. Trade-deadline futures offer information-rich pricing — strong if you can identify which deadline acquisitions will translate to playoff success and which are window-dressing. A balanced futures bankroll holds at least one pre-season position and at least one post-deadline position, sized to the conviction behind each.